Key Takeaways

- Northern Miner recently unveiled the ranking of the world’s largest copper mines, spotlighting the significant players shaping the global copper market.

- As the mining industry navigates through 2026, these rankings provide critical insights into operational capacities and geopolitical factors influencing the copper supply chain.

- Understanding the Rankings: Who Tops the List?

Northern Miner recently unveiled the ranking of the world’s largest copper mines, spotlighting the significant players shaping the global copper market. As the mining industry navigates through 2026, these rankings provide critical insights into operational capacities and geopolitical factors influencing the copper supply chain.

Understanding the Rankings: Who Tops the List?

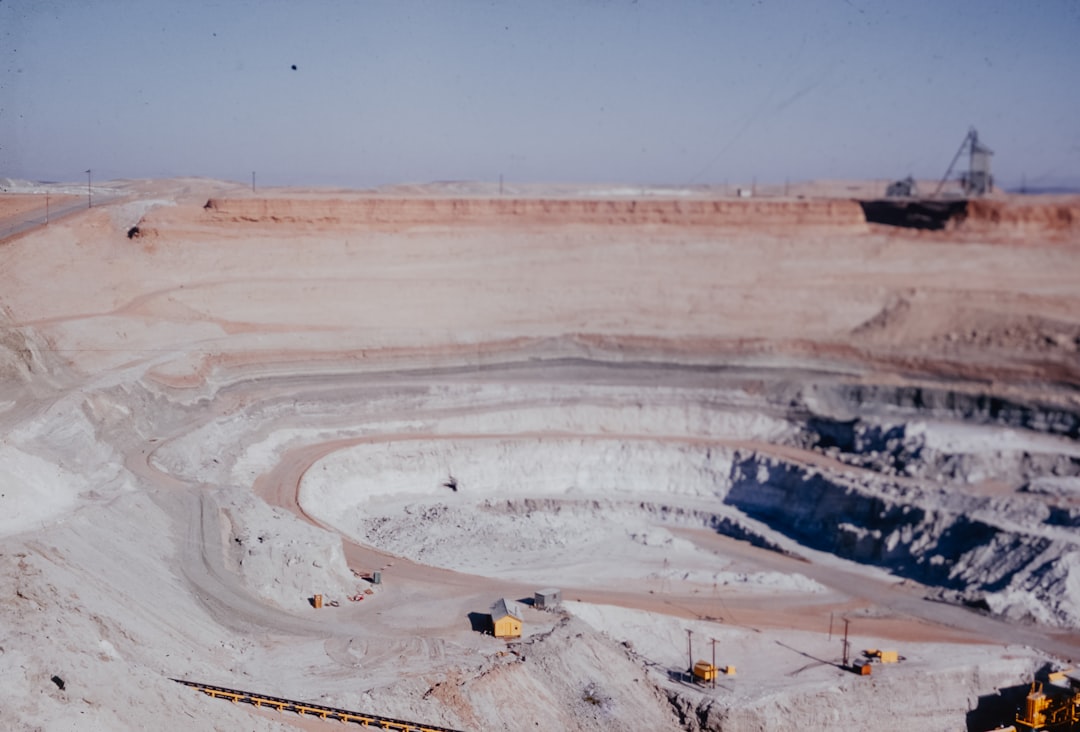

The latest rankings highlight the dominance of certain mining giants in the global copper industry. Amidst a backdrop of geopolitical uncertainty and fluctuating demand, these mines are not only pivotal in terms of production volume but also in setting industry benchmarks. The list features prominent names such as Escondida in Chile, operated by BHP and Rio Tinto, and Grasberg in Indonesia, managed by Freeport-McMoRan. These operations are crucial, as they collectively represent a significant portion of the world’s copper output.

Escondida, for instance, remains the world’s largest copper mine by production, contributing over one million tonnes annually as per BHP’s 2025 annual report. This mine’s consistent output underscores its resilience amidst market volatility. Similarly, Grasberg’s ongoing expansion and transition to underground development have been pivotal, as noted in Freeport-McMoRan’s Q1 2026 earnings call, which highlighted continued investment in its infrastructure.

Market Dynamics: Copper’s Critical Role

The importance of copper in today’s market cannot be overstated. As a critical mineral, copper’s demand is driven by its extensive use in renewable energy technologies and electric vehicles. The International Copper Study Group (ICSG) reports global copper demand is projected to rise by 3.2% in 2026. This demand is further fueled by governmental policies in the U.S. and Europe aimed at reducing carbon footprints, creating a robust market for copper.

However, the threat of tariffs, particularly from the United States, poses a potential risk. The tariffs could disrupt supply chains, increasing operational costs for producers and affecting global copper prices. Such geopolitical tensions have historically led to price volatility, as evidenced by the fluctuations seen in copper prices on the London Metal Exchange (LME) in recent years.

Investor Implications: Navigating a Volatile Landscape

From an investment perspective, these rankings and the broader market dynamics present a complex but potentially rewarding landscape. The resilience of top-tier mines like Escondida and Grasberg suggests a stable return for stakeholders amidst market uncertainties. However, investors must remain cautious of geopolitical developments and their impact on production costs and global trade flows.

The transition to greener technologies presents a double-edged sword. While it promises increased copper demand, it also pressures mining companies to adopt sustainable practices, potentially increasing operational expenditures. According to a recent report by the International Energy Agency (IEA), mining operations are under increasing scrutiny to align with environmental standards, which could drive innovation but also necessitate significant investment.

As we move through 2026, the global copper market is poised for transformative changes. Mines that can adapt to evolving geopolitical, economic, and environmental landscapes will likely define the next era of the copper industry. Investors and industry stakeholders will need to navigate carefully, balancing opportunities with inherent risks, to capitalize on copper’s critical role in the global economy.</p

Source: Northern Miner

Editorial Note: This article is an independent analysis based on publicly available information and press releases. MineListings.com is not affiliated with the companies mentioned. The views expressed are those of our editorial team and do not represent the official position of any company discussed. For the most accurate and complete information, readers should refer to the original source materials and company filings.

Sources: This article synthesizes publicly available filings, exchange data, and government reports as cited.